Personal Accident cover helps beneficiaries or policyholders in gaining financial compensation during injury, disability, or death caused due to accident. However, there are various limitations & benefits to claiming personal accident coverage. Check out this article to know the possibilities of coverages, benefits, limitations, & personal accident cover claiming process.

What Is Personal Accident Cover?

Personal Accident Cover is a type of insurance that provides financial compensation to the policyholder or their beneficiaries in case of an accidental injury, disability, or death.

This coverage is usually offered as a standalone policy, but it can also be added as a rider or add-on to a life insurance policy.

Personal Accident Cover typically provides benefits such as a lump sum payment for accidental death, a lump sum payment for permanent total disability, and a weekly or monthly benefit for temporary total disability.

Some policies may also cover medical expenses incurred due to an accident.

The sum assured, or the maximum amount that the insurance company will pay in case of a claim is chosen by the policyholder.

The premium for Personal Accident Cover depends on factors such as the sum assured, the age of the policyholder, occupation, and lifestyle.

Personal Accident Cover is essential for individuals who have a higher risk of accidents due to their profession or lifestyle, such as athletes, construction workers, or frequent travelers.

It can also provide financial security for families who depend on a single-income earner.

It is important to note that Personal Accident Cover only covers accidents and not illnesses or natural death. Therefore, it should not be considered a substitute for health insurance or life insurance.

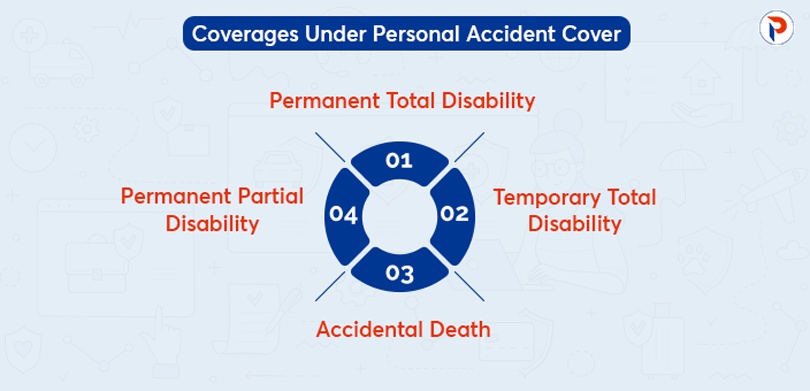

Coverage of Personal Accident Cover

Personal accident cover provides coverage for the following:

- Accidental death: If the policyholder dies in an accident, the insurance company pays a lump sum amount to the nominee of the policyholder.

- Permanent total disability: If the policyholder becomes permanently disabled due to an accident, the insurance company pays a lump sum amount as compensation.

- Permanent partial disability: If the policyholder becomes partially disabled due to an accident, the insurance company pays a percentage of the sum assured as compensation.

- Temporary total disability: If the policyholder becomes temporarily disabled due to an accident, the insurance company pays a weekly or monthly benefit amount as compensation.

- Hospitalization expenses: If the policyholder is hospitalized due to an accident, the insurance company pays for the medical expenses incurred during the hospitalization.

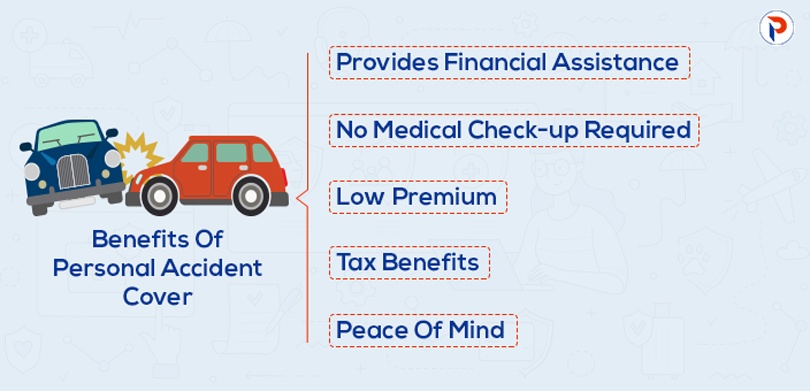

Benefits of Personal Accident Cover

Following are the benefits of personal accident cover provided for the

- Financial assistance: Personal accident cover provides financial assistance to the policyholder in case of an accident. The policy ensures that the policyholder and his/her family members are protected from the financial burden of medical expenses and loss of income due to an accident.

- Peace of mind: Personal accident cover provides peace of mind to the policyholder and his/her family members. The policy ensures that they are financially protected in case of an accident.

- No medical check-up required: Personal accident cover does not require a medical check-up. The policy can be purchased online or offline without any medical examination.

- Low premium: Personal accident cover is a low-cost insurance policy. The premium for the policy is relatively low compared to other insurance policies.

- Tax benefits: Personal accident cover provides tax benefits under section 80D of the Income Tax Act, 1961. The policyholder can claim a tax deduction of up to Rs. 25,000 for the premium paid towards the policy.

Limitations of Personal Accident Cover

Following are the limitations of the personal accident cover

- Limited coverage: Personal accident cover provides limited coverage. The policy covers accidents only and does not cover illnesses or diseases.

- Exclusions: Personal accident cover has certain exclusions. The policy does not cover accidents due to pre-existing conditions, self-inflicted injuries, or injuries caused by participating in hazardous activities.

- Limited sum assured: Personal accident cover provides a limited sum assured. The policyholder cannot claim more than the sum assured in case of an accident.

- Limited duration: Personal accident cover has a limited duration. The policy is valid for a specific period, after which the policyholder needs to renew the policy.

What Is Personal Accident Cover In Bike Insurance?

There are chances that you, your bike & third parties get damaged by meeting accidents on the road.

The damage faced by a third party because of you are counted under the third-party insurance policy. Let it be an injury to a person or damage that happened to the vehicle.

Whereas, comprehensive policy holds all of the damages, let it be faced by you or a third party. And in this scenario, personal accident cover comes into existence.

If the personal accident cover is under the insurance policy, the owner or driver of the bike will be eligible for seeking cover.

You can check out What Are Different Types of Motor Insurance? to know the importance & types of Motor insurance available.

What Is Personal Accident Cover In Car Insurance?

The personal accident cover in a car insurance policy includes accidental injuries, permanent total disability & partial disability with other benefits.

Accident scenarios mentioned in Personal accident car insurance are

- Any type of road, rail, or aerial accident.

- Any type of injuries that happened due to the cylinder burst.

- Injuries occurred because of drowning, burning, poisoning, etc.

- Injuries occurred because of falls or collisions.

Document Required To Claim During Policy Holder’s Accidental Death

Arrange and submit the following documents to claim the insurance during the policyholder’s accidental death.

- Death Certificate

- Original Policy Documents

- Policyholder’s age proof

- ID Proof of Beneficiary

- Medical certificate

- Police FIR (during unnatural death scenario)

- Discharge form

- Hospitals records (during death because of illness)

- Post-mortem report (during unnatural death)

- Employer & cremation certificate

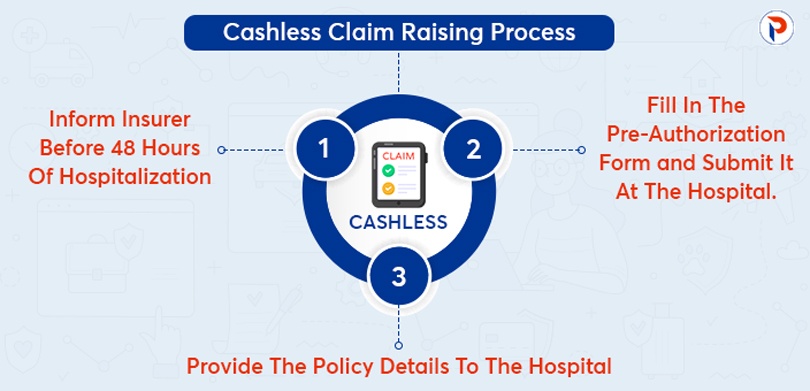

How To Raise Cashless Claim?

Cashless treatment can be done through partner network hospitals in India. However, during an accident, approaching the nearest hospital is the best option.

If you are clear about the network hospitals of the insurer & you can reach one of them then you should reach the nearest one.

Follow the below-mentioned process to claim in this scenario.

Step 1:

You should inform the insurer before 48 hours of hospitalization.

Step 2:

Provide the policy details or policy cashless card of the patient at the insurance desk of the hospital with valid ID proofs.

Step 3:

Fill in all the details asked in the pre-authorization form. And submit the form at the hospital.

Step 4:

For early response, fill out the request form by visiting the official portal of the insurer. And inform the same to insurer.

Step 5:

The insurance provider will take up to 2 hours to review your application & inform you about the same through SMS & email.

Step 6:

You can also check the claim status online.

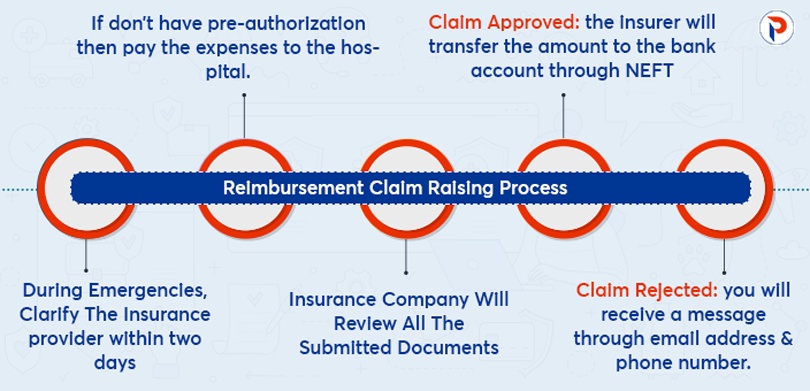

How To Raise Reimbursement Claim?

Follow the below-mentioned steps to raise a reimbursement claim.

Step 1:

During emergencies, you will need to clarify the insurance provider in the upcoming two days. And pay the expenses to the hospital if you don’t have pre-authorization.

Step 2:

Arrange & submit the all necessary documents in the upcoming 15 days of discharge.

Step 3:

The insurance company will review all the submitted documents & decide to reject or accept the claim.

Step 4:

If the claim is approved then the insurer will transfer the particular amount to the registered bank account through NEFT.

Step 5:

If the claim is rejected then you will get a message about the same through the registered email address & phone number.

FAQs

| What is the coverage under personal accident cover?

Accidental death, permanent total disability, permanent partial disability, temporary total disability, & hospitalization expenses are the coverages provided under personal accident cover. |

| What are the benefits of personal accident coverage?

Financial assistance, no medical check-up required, low premiums, Tax benefits, etc are some of the benefits of personal accident coverage. |

| What are the limitations of personal accident coverage?

Limited sum assured, limited duration, limited coverage, etc are some of the limitations of personal accident cover. |

| Is personal accident coverage similar to health insurance?

It is important to note that personal accident cover only covers accidents and not illnesses or natural death. Therefore, it should not be considered a substitute for health insurance or life insurance. |

{kind=link}